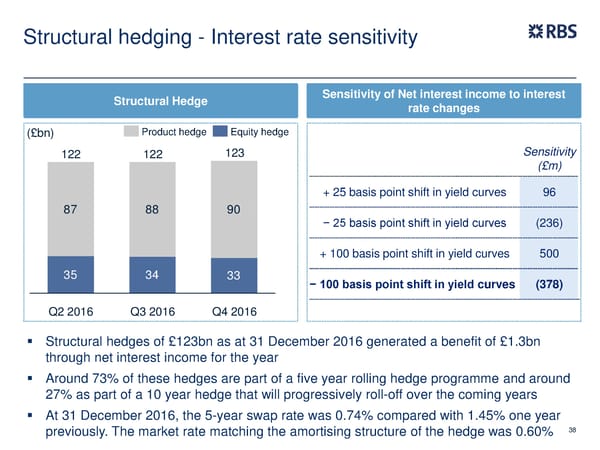

Structural hedging - Interest rate sensitivity Structural Hedge Sensitivity of Net interest income to interest rate changes (£bn) Product hedge Equity hedge 122 122 123 Sensitivity (£m) + 25 basis point shift in yield curves 96 87 88 90 − 25 basis point shift in yield curves (236) + 100 basis point shift in yield curves 500 35 34 33 − 100 basis point shift in yield curves (378) Q2 2016 Q3 2016 Q4 2016 Structural hedges of £123bn as at 31 December 2016 generated a benefit of £1.3bn through net interest income for the year Around 73% of these hedges are part of a five year rolling hedge programme and around 27% as part of a 10 year hedge that will progressively roll-off over the coming years At 31 December 2016, the 5-year swap rate was 0.74% compared with 1.45% one year previously. The market rate matching the amortising structure of the hedge was 0.60% 38

FY Results | RBS Group Page 37 Page 39

FY Results | RBS Group Page 37 Page 39