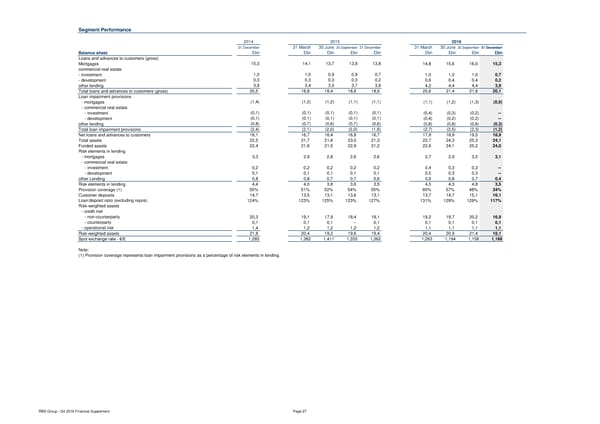

Segment Performance 2014 2015 2016 31 December 31 March 30 June 30 September 31 December 31 March 30 June 30 September 31 December Balance sheet £bn £bn £bn £bn £bn £bn £bn £bn £bn Loans and advances to customers (gross) Mortgages 15,3 14,1 13,7 13,9 13,8 14,8 15,6 16,0 15,3 commercial real estate - investment 1,0 1,0 0,9 0,9 0,7 1,0 1,0 1,0 0,7 - development 0,3 0,3 0,3 0,3 0,2 0,6 0,4 0,4 0,2 other lending 3,9 3,4 3,5 3,7 3,9 4,2 4,4 4,4 3,9 Total loans and advances to customers (gross) 20,5 18,8 18,4 18,8 18,6 20,6 21,4 21,8 20,1 Loan impairment provisions - mortgages (1,4) (1,2) (1,2) (1,1) (1,1) (1,1) (1,2) (1,3) (0,9) - commercial real estate - investment (0,1) (0,1) (0,1) (0,1) (0,1) (0,4) (0,3) (0,2) -- - development (0,1) (0,1) (0,1) (0,1) (0,1) (0,4) (0,2) (0,2) -- other lending (0,8) (0,7) (0,6) (0,7) (0,6) (0,8) (0,8) (0,6) (0,3) Total loan impairment provisions (2,4) (2,1) (2,0) (2,0) (1,9) (2,7) (2,5) (2,3) (1,2) Net loans and advances to customers 18,1 16,7 16,4 16,8 16,7 17,9 18,9 19,5 18,9 Total assets 22,5 21,7 21,6 23,0 21,3 22,7 24,3 25,3 24,1 Funded assets 22,4 21,6 21,5 22,9 21,2 22,6 24,1 25,2 24,0 Risk elements in lending - mortgages 3,3 2,9 2,8 2,6 2,6 2,7 2,9 3,5 3,1 - commercial real estate - investment 0,2 0,2 0,2 0,2 0,2 0,4 0,3 0,3 -- - development 0,1 0,1 0,1 0,1 0,1 0,5 0,3 0,3 -- other Lending 0,8 0,8 0,7 0,7 0,6 0,9 0,8 0,7 0,4 Risk elements in lending 4,4 4,0 3,8 3,6 3,5 4,5 4,3 4,8 3,5 Provision coverage (1) 55% 51% 52% 54% 55% 60% 57% 48% 34% Customer deposits 14,7 13,5 13,1 13,6 13,1 13,7 14,7 15,1 16,1 Loan:deposit ratio (excluding repos) 124% 123% 125% 123% 127% 131% 129% 129% 117% Risk-weighted assets - credit risk - non-counterparty 20,3 19,1 17,9 18,4 18,1 19,2 19,7 20,2 16,9 - counterparty 0,1 0,1 0,1 -- 0,1 0,1 0,1 0,1 0,1 - operational risk 1,4 1,2 1,2 1,2 1,2 1,1 1,1 1,1 1,1 Risk-weighted assets 21,8 20,4 19,2 19,6 19,4 20,4 20,9 21,4 18,1 Spot exchange rate - €/£ 1,285 1,382 1,411 1,355 1,362 1,263 1,194 1,158 1,168 Note: (1) Provision coverage represents loan impairment provisions as a percentage of risk elements in lending. RBS Group - Q4 2016 Financial Supplement Page 27

Financial Supplement Page 26 Page 28

Financial Supplement Page 26 Page 28